In November of this year, my personal portfolio made an all time high. The previous time I had seen an all time high was way back in early January of 2018. A couple of months, it would have been three years since I last made an all time high for the portfolio (not inclusive of dividends though).

Equity returns are lumpy in nature. Unfortunately most of us don’t have the patience to hold through the worst of times in preparation for the oncoming best of times. Fear has a way of playing its tricks on our mind at the worst possible times.

Markets loathe giving free money to one and all. Before the 2008 financial crisis led crash, Indian Markets used to crash once in two years on an average. When I say crash, I mean a drop of at least 30% from the previous peak.

In 1996, Nifty 50 rose from 800 to 1200 by the middle of the year but by the end, it was down 800. In 1997, it once again rose to 1300 just to fall back to 950 by early January 1998. The bounce 1200 odd before jettisoning all the gains and falling back to 800 by late 1998. From there started the Dot Com bubble rally that took Nifty 50 to 1800 levels before the crash took it over time back to 920 in late 2001.

Then we had the crash of 2004, 2006 and of course, the crash of 2008. Post 2008, Markets drifted lower for a considerable length of time only once – 2011 and even then did not go below the 30% mark. In fact, after 2008, March 2020 was the first time we saw a drawdown greater than 30%.

The financial crisis and the way the Federal Reserve responded has changed the behavior of the market. Just when it seemed the normalcy of balance sheets of the Central Bank will be restored, we were hit with Covid which has resulted in an unprecedented flow of liquidity.

While the recent rise in Indian Equities thanks to the generous inflow of funds from FII’s, do note that India is the only country into which liquidity is pouring. For most other emerging markets, its the other way round. To me, this is indicative that much of the flow may not be speculative in nature and at least a large part could be because of a change in perception with regards to the future growth of the economy.

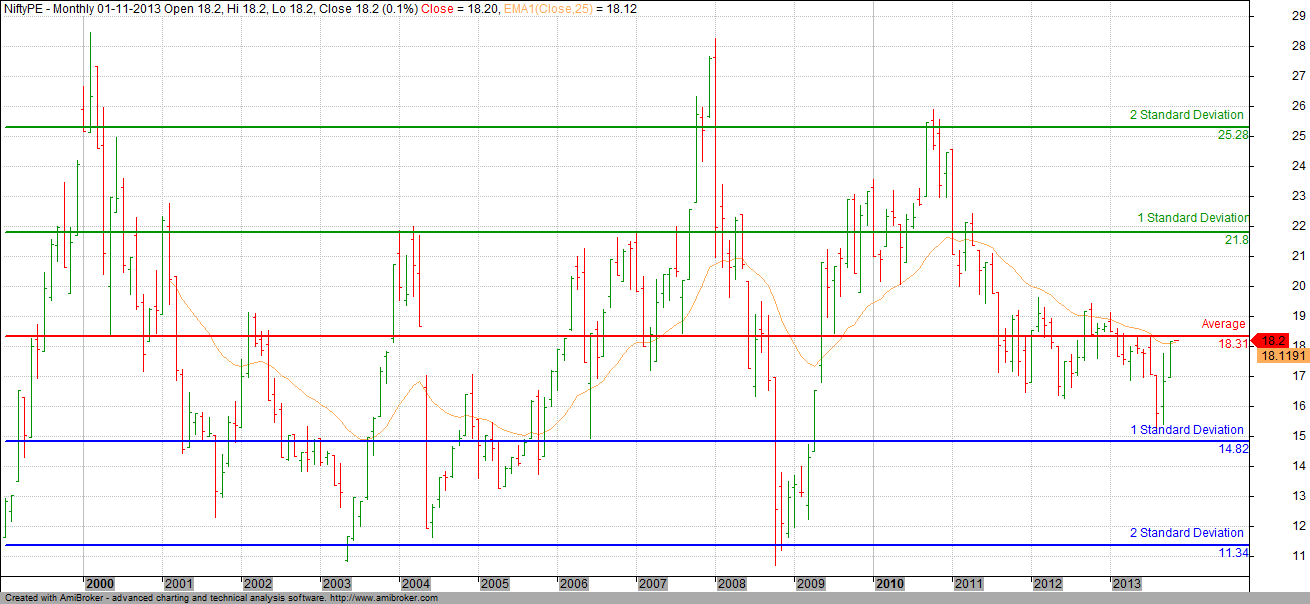

Markets are expensive, goes the headline. Most measure the valuation of the market by using Nifty 50 Trailing Price to Earning as the proxy. But why Nifty 50 and why not Sensex or the Nifty 500 or the Price Earnings of the market as a whole. Is it because we all have fallen prey to availability bias?

In 2020, Sensex went up by 15.8%, Nifty 50 by 14.90%. Sensex Price to Earnings on the other hand went up by 28.80% while Nifty 50 PE went up by 35.90%. At the end of the year, Nifty PE stood at 38.45 vs Sensex PE of 33.50. Would you say Sensex is cheaper than Nifty?

No one knows the future but one can be pretty confident that the earnings of companies for the financial year 2021-2022 will be way better than 2020-2021. How much better would make it easy to get a fix on how expensive the market really is. Oh, by the way Nifty PE is Standalone earnings while the true picture will be shown by using Consolidated earnings. But since NSE doesn’t provide it, we don’t bother with it.

Then there is Authority Bias. We stop questioning things just because someone with authority says so and if he says so, how could it be wrong. So, when claims are made using a single example of who SIP is better than Lumpsium, we don’t stop to question the stupidity of comparing an Apple with a Pineapple.

Questions are always asked of a bull market – be it at the beginning, the middle or the end. There will always be some indicator or parameter that can be used to defend a bull case or make a bear case. In Statistics, one school of thought says that if you have at least 30 independent samples, it can be used to make some decent predictions. We end up making predictions with a sample size of two or three and then wonder why we went wrong.

Equity is Risk when looked at a short term time frame. There is no getting away from it. If you invest money today, the risk to capital exists at the very least for one year if not more. But as time passes, the risk moves on from the capital invested to the gains and as one moves even further, it’s just part of the gains that will be at risk.

The longer you stay in the markets, lower the risks of ruin (unless of course you are leveraged in which case, the risk of ruin may never go). But to stay longer, you should invest only so much that allows you the comfort of good sleep regardless of market conditions. A secondary requirement of course is to invest in something you deeply understand or trust. The reason I could stay with the strategy during its long drawdown had more to do with my trust rather than any superior skill sets. Building that takes time but once built, it serves you for the lifetime.