Its been 9 months (nearly) since I wrote this post (link) and markets in the meantime has appreciated (with a couple of glitches on the way) by around 15%. A FD on the other hand would have yielded at best 6.75% and hence markets have for now hands down beaten my view of FD being a better bet (though since at one point we were down 8.5% from the point I wrote thus gives me some hope 😛 )

Before I write, a quote from the Oracle of Omaha which appeared in his recent annual Report

<Quote>

Forming macro opinions or listening to the macro or market predictions of others is a waste of time.

Indeed, it is dangerous because it may blur your vision of the facts that are truly important. (When I hear TV commentators glibly opine on what the market will do next, I am reminded of Mickey Mantle’s scathing comment: “You don’t know how easy this game is until you get into that broadcasting booth.”)

<End Quote>

Of course, since Buffett has broken nearly every rule he has advocated, I am still hopeful that some day he may come around to accept that every investor and trader needs to have a macro view (regardless of whether one wants to implement it or not) 🙂

Last three weeks has been hectic for the markets with Nifty gaining around 7.8%. While 7.8% in itself is not a great achievement, the fact that we have broken the all time high is leading to a lot of bullish talk (compared to say in Jan – Feb of 2012 when we logged positive gains for 7 consecutive weeks which totally gave a gain of 19%) especially since this is a news driven (Election / Modi) rally than one based on pure fundamentals.

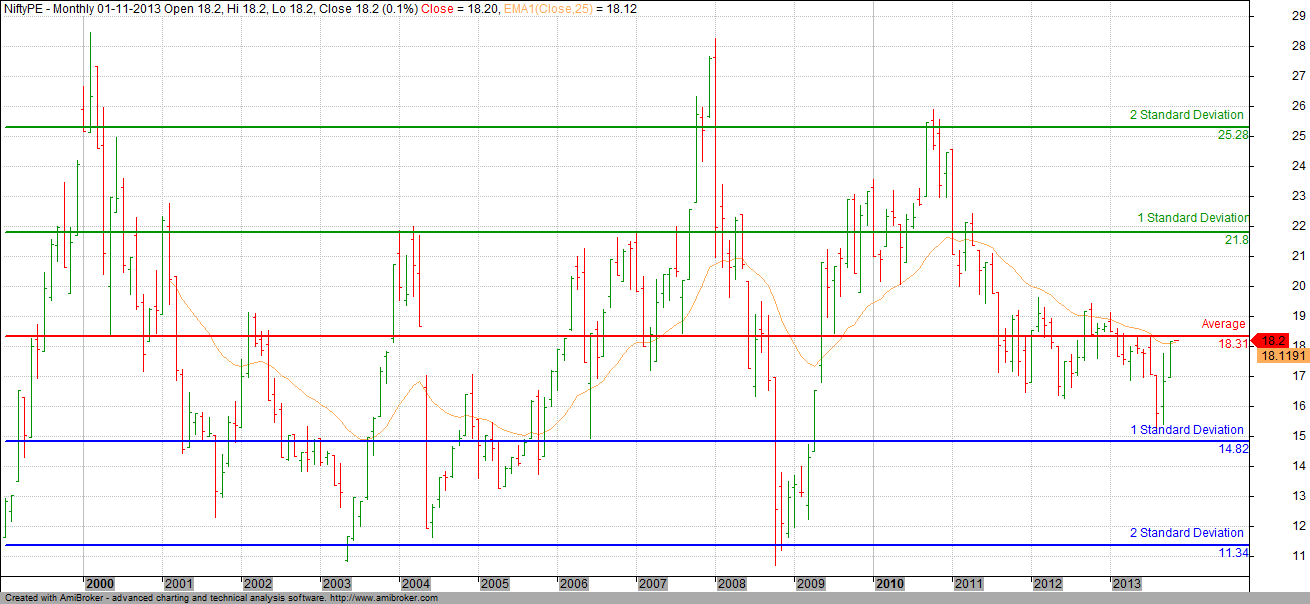

That is not to say, fundamentals aren’t showing any great promise. If one were to look at the Nifty PE Ratio (Standalone), we are at the median range – neither expensive nor cheap and this indicates that any upside from here will have fundamental blessing as well (any fall with make the market cheap & hence making it even more of a Buy)

Since the key driver to the markets for the time being is the Elections, let me Analyse how markets behaved prior to the previous two elections (when we had some amount of euphoria).

NDA called for early elections in January 2004 and the results were out in May. Here is the Gains / Losses of Nifty on a monthly time frame.

| Month | Change |

| Jan-04 | -3.9 |

| Feb-04 | -0.6 |

| Mar-04 | -2.2 |

| Apr-04 | 1 |

| May-04 | -17.9 |

While on the face of it, it looks like the markets were slightly bearish going into the elections, one has to understand the larger context as well. Nifty after being bearish for 3 years since the Dot Com bust had recorded a rise of 73% in 2003. Hence the first few months of non performance could actually be seen as a consolidation playing out (especially since market was sure of a NDA victory). But we know how the story happened in reality.

2009 was a different case altogether with the 2008 crash still being fresh and markets worldwide were already revving up. Election dates were as this time around announced in March and results came in May. Since we looked at 5 months in 2004, lets look at the same 5 months in 2009

| Month | Change |

| Jan-09 | -2.9 |

| Feb-09 | -3.9 |

| Mar-09 | 9.3 |

| Apr-09 | 15 |

| May-09 | 28.1 |

Markets worldwide bottomed out in March and started to move higher and hence our move in March and April can be attributed to that rather than election euphoria. The rise in May (where we saw markets frozen for the first time on the upper circuit) to me was more of a managed move than a move where participation was high.

Coming back to the present situation. My belief (based on my reading) was that BJP (Modi) would find it difficult to come to power. The current market move though has been based on evidence that is pointing out to the contrary. Yesterday I was talking to a person who is biased towards BJP (being a party worker) and he claimed that their caclulation was that there was very high probability of NDA making it across 300. Now, I do not know how the figures have come, but its sure that UP seems to be seen as the game changer.

In the last decade, we had 2 major bull rallies – 2003 and 2009. One way of anticipating the next would be to see how markets had performed before the period and whether we can see a similar situation now.

One way of doing it would be to look at 10 year rolling returns. On the Sensex (using it instead of Nifty due to the longer amount of data we have), we can see that at end of 2002, the 10 Year rolling returns had slipped to 0.93%. At end of 2008, 92.72%. At the end of 2013, the same is 220.64%.

Lets look at 5 year rolling returns. At end of 2000 (after the bust of Dot Com), the number was 1.15% while the same as of end of 2013 is 4.36% (lowest since 2001). The average of the 10 year rolling returns comes to 380% with Standard Deviation at 285. In a way, we are below the mean, but not below or even close to 1 Standard Deviation. In 2009, we were close to 1 Standard Deviation and in 2003 we were way below that.

A swing projection of Nifty seems to suggest to me that the current move can extend to around 6850 at the very least, but then again, its just a projection prone to error (though it has had its good days including projecting the likely low in Aug 2013 – we came pretty close before bouncing back.)

While anything can happen in markets, I am still wary of a run away bull market from this point on-wards without there being a long pause in between. For now though, if you aren’t a bull, you are missing it 🙂

As a saying goes (attributed to Keynes, but disputed). When the Facts Change, I Change My Mind. What Do You Do, Sir