On Twitter, its amazing to see the number of winners who seem to be right in whatever trade they report (mostly after the move) and in an attempt to get them to commit to something, commented that I was going into the election result day with “Long Nifty” positions.

Good friend, Nitin of Alpha Ideas replied back with a quote by “Paul Tudor Jones” and I quote the same here

“I don’t risk significant amounts of money in front of key reports, since that is gambling, not trading”

Now, unlike the hundreds of quotes available, this is from a guy who is seen as one of the Top Technical Analysts ever (Link) and hence something that cannot be dismissed off hand (as I generally tend to do). This guy has some serious skin in the game (as against the guy who invented that term but seems to spend more time talking than trading – but that is for later:) ).

In many ways, trading is generally seen as Gambling though the gulf between gambling and trading is as wide as the Brahmaputra at its widest point. A gambler is one who takes risk with not much of a risk management and generally in a place where the odds of winning are pretty low.

The big question out here is, If I am positioned for the election result – am I gambling or this is as normal a trade as any other I take? To answer that, let me give you the thought process that made me willing to bet (and I generally bet as much as I can afford – no half measures out here) and why I believe that if one looks at history (and TA is all about the history repeating itself), betting on the long side is the way to go.

I am a believer in positional systematic trading and believe that intra-day trading or discretionary trading (gut based or based on ideas that cannot be historically tested to see its accuracy) is not the way to go. I am also a strong believer in trend following since evidence has shown that all said and done, for some reason that is as yet not explained, trends do persist more often than they are supposed be.

The big profits of a trend follower come from the outlier’s – moves that are 3 / 4 or even 5 standard deviation from the mean and which theoretically should not occur in decades or centuries but which happen more often that not. Its the outlier that ensures the profitability (extra Alpha if I may say) of a trend following system since it generally has more loss making trades than profit making and these one off trades more than compensate for all the losses.

Outliers can occur due to various reasons – Known events and Unknown events. Election results are a known event since regardless of what happens, results will be out by day’s end. On the other hand, a attack on the World Trade Towers in 2001 was an Unknown event since no one knew such a thing could happen.

A couple of years back, I had given a talk on Trend Following and showcased as to how markets seemed to be perfectly aligned with the post event trend even though in case of unknown events, the very event was a surprise. Let me take you through some of the examples I provided in that talk

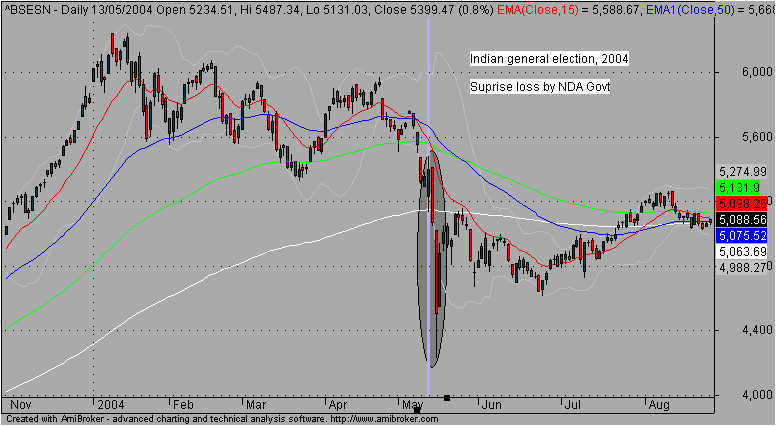

1. Fall of BJP led NDA Govt in 2004

As can be seen, in the run up to the results, despite the euphoria of “India Shining”, the markets were considerably weak. Markets closed with small gains on result day and tumbled in the next couple of days.

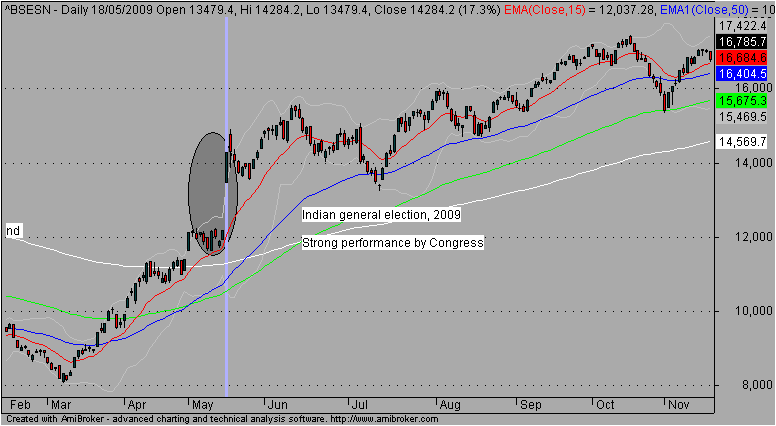

2. UPA wins the election in 2009

Now, this was supposed to be so big a surprise (especially that of Congress along mopping up >200 seats) that Index froze higher. But look at the chart and say that the trend was anything other than bullish

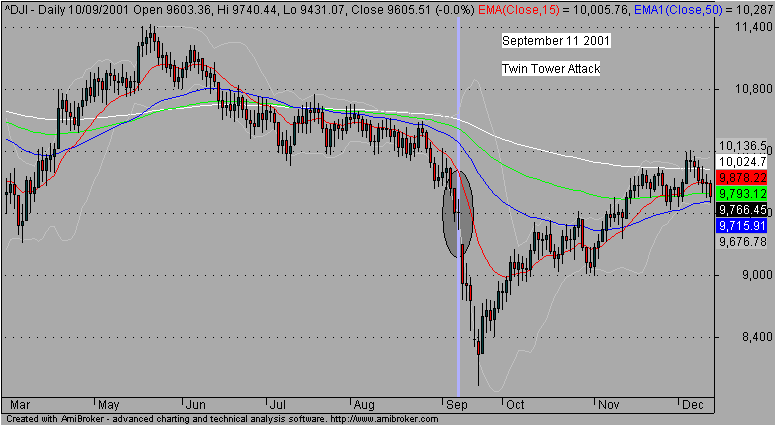

3. Terrorist Attack on World Trade Towers

Now, this was a unknown unknown event of a magnitude not seen in a very long time and yet, Dow was strongly bearish before the event and the only thing that this did was accelerate the fall when markets re-opened.

4. Great Hanshin earthquake, Kobe Earthquake

Japan was rattled by the Kobe earthquake and in a in-direct way was the cause of the fall of Barings Bank (Nick Leeson). One look at the Nikkei chart above, the trend was already present and in fact, it was only 2 days after the earth quake happened that Nikkei started to crack strongly.

5. Russia Bond Default

Russia in 1998 defaulted on its own loan and this in a way shook the world markets then. The default was the key catalyst to the end of one of the biggest hedge funds of that time – Long Term Capital Management. Look at the trend and say that the markets had no clue about it

I believe if one were to dig deep, one can find even more examples of how the markets were most of the time in line with the trend well before the event and the event in itself was not a surprise to anyone other than maybe those in the media.

My own bet on the markets today has been based on a system I trade and has been tested both historically and in real time for quite some time now. Add to it, unlike 2009, this time around, the trends and the results will be during market time and shall not be a surprise at the open.

Its easy to rationalize as to why one should not trade before key events, but as I have shown in the examples above, if you are with the trend, there is little to fear about.