Mutual funds are one of the ideal vehicles to invest in the markets. But with a plethora of funds, its tough to identify what fund to go with. Should one invest in the top rated (by rating agencies such as ICRA) or should one invest in funds managed by star managers.

Among the large cap funds, HDFC Top 200 fund rules the roost. With Asset under Management of 14,285 Crores, its one of the biggest (if not the biggest) funds that you can find in India. Launched in 1996, the fund has a very impressive track record with compounded growth of 22.37% since launch. The expense ratio for the fund is 2.33% for the regular plan and 1.65% for the Direct plan.

Two funds that have a similar history (in terms of being launched around the same time) come from the Templeon stable.

First off was the Kothari Templeton Prima Fund (as it was called in those days). Launched in 1993, it has been one of the top performing funds with it having a return since launch of 21.80%. But despite such stellar returns, its Asset under Management is just around 3400 Crores. Expense ratio for the fund is 2.32% for the regular plan and 1.14% for the Direct (among the lowest you shall come across).

A year later, the fund house launched another fund – Kothari Templeton Prima Plus. The return for this fund since launch is 20.36% which while lower compared to the above two funds, is still way above many other funds with similar length of operation. For example, State Bank of India launched its SBI Global 94 fund in the same period and the return for that fund since launch has been just 16.08%

To close off, we shall analyze another fund that started off as the first Direct only plan and remains Direct only till date. It has one of the lowest expense ratio’s of 1.25% on assets. While the performance as we shall see has been better than HDFC Top 200 fund, its Assets under Management is a partly 416 Crores. The fund started off only in 2006 and hence the data history is limited compared to that of HDFC Top 200

To make it even, I shall analyze the funds starting from 1st April 2006 to make all of them comparable as well as to provide a better understanding of the risks one saw when the markets dipped in 2008.

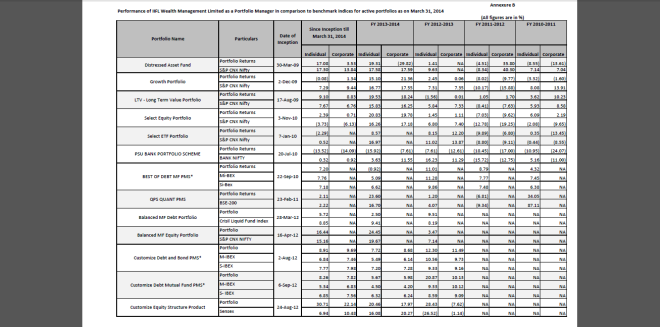

First off, a comparison chart of the above funds.

(click on the above chart to get the full picture)

(click on the above chart to get the full picture)

As can be seen, all the funds have beaten the benchmark (Nifty Total Return Index) by a pretty significant margin. In a way, this points out the advantage of actually investing in a fund versus investing in a ETF that tracks the benchmark index. Then again, since all these funds have investments in Mid and Small Cap firms), the logic of using Nifty as a benchmark in itself maybe faulty. But since we do not have the data (Total Return Index of CNX 500), we cannot but compare with what we have got.

While its clear that the funds have performed way better than the benchmark, what a investor should look at is how they performed when markets literally fell through in 2008 / 09. Since Mutual funds need to hold a minimum of 70% of their assets in stocks, when markets crash, they too unfailingly start falling though depending on how good the allocation of the fund manager is, some funds maybe better off than others.

For instance, right now, Quantum Long Term Equity Fund has its max level of cash (nearly 30%). In the event markets crash, this amount cash not only means a lower draw-down but also the fund manager is not compelled to sell stocks at their lows due to investor withdrawals.

While CNX Nifty touched its low in late October of 2008, we shall take the low of March 2009 (right before markets took off) to see how much the funds lost compared to the Index.

In the chart above, what you see is that when markets made their final bottom in 2009, it was performing much better than the Templeton twins. A near 70% draw-down in Prima Plus seems to suggest that while funds perform brilliantly in bull markets, thanks to moves in mid and small cap stocks, when one hits a bear market, its those very stocks that drag the performance to hell.

With markets being strongly bullish, investors are once again rushing to invest into mutual funds. A quote from a recent article in Mint shows how bullish Indians have become in the just concluded financial year compared to 2008

Mutual funds (MFs) invested a record Rs.38,627 crore in Indian stocks in the year to 31 March—more than double the previous highest in the year ended March 2008

Even investments into Portfolio Management Schemes has shot up substantially, but as the above data shows, the question that should be asked is, are investors prepared to wait it out in case things do not turn out as anticipated. After all, markets are not a one way street to riches but a way to channel earnings for a better return in the long term than one that can be achieved elsewhere.

Investing by just looking at performance can be risky if such performance was delivered by taking higher risks. One needs to understand that while there is always a give and take relationship, when the shit hits the fan, all kinds of logical thinking are quickly thrown out of the window with investors keen to get out at any rate possible regardless of the fact that cycles are common and one never knows when this will end and the next begins.