Not a day goes by these days without someone commenting that the market is ripe for a correction. After all, the economy as we see it through our eyes is worse than at any point we have come across in the past and yet the stock market is rocking. It’s a conundrum that is confusing the best of investors.

The Nifty 50 PE ratio which is seen as more representative than the BSE Sensex PE ratio is now at an all time high. The Sensex PE Ratio while not at an all time is currently around the same level where we saw it in January 2008. But the consensus that one comes across seems to suggest that looking at PE ratio is faulty since the drop in earnings which has subsequently boosted the Price to Earning Ratio is a one off due to the compulsory closure of much of the country in Quarter 1 of 2020. The impact of this quarter’s damage will get wiped out in years time, but the question is where will the Indices be by that juncture.

This dichotomy between stock markets and the economy is not being seen only in India. In fact, S&P 500 – the barometer stock index in the United States made a new high this week. This while even the US is suffering immensely from the damage caused by Covid. This from a New York time post

“The Federal Reserve Bank of New York’s weekly economic index suggests that the economy, although off its low point a few months ago, is still more deeply depressed than it was at any point during the recession that followed the 2008 financial crisis.”

While Robinhooders, the moniker attached to small retail investors who trade through the RobinHood Application has been blamed for exacerbating the relentless rise, the fact remains that we, the small retail investors are generally the weak hands. Yes, once in a while we get it right while the highly paid Institutions get it wrong, but for most of the time it’s the opposite.

Since November 2013, we have seen just 3 months where Net Equity Inflow was negative for Mutual Funds. The first was in March 2014, next came in March 2016. June 2016 was another negative month but could be ignored given that outflow was just 45 Crores. The last outflow has come in the last month – July 2020.

The question that needs to be asked is if smart retail is turning out to be ahead of the crowd. The reason for using the smart prefix is because even in July, we saw Inflows of 14 thousand Crores. It’s just that more money was withdrawn resulting in Net negative for the month.

Between the months of January 2008 to March 2008, Mutual funds saw an inflow of around 24000 Crores. Rest of the year basically was flat even though markets kept getting cheaper. In fact, the biggest outflow for 2008 was in October when markets hit its lowest level. On the other hand, when markets recovered, retail started to sell back with total net outflows between September 2009 to October 2010 being to the tune of 24000 Crores. Nifty though did not waver much as it continued its upward journey.

Nifty has been on a major uptrend since 2009 and yet for anyone who has been invested for the last 7 years, returns have been suboptimal leading one to wonder that with all the problems that surround us, are we better off with a lower exposure today than before.

The question hence is where we do go from here. I wish I knew the answer. On one hand there have been serious reports suggesting that we may be on the cusp of a new bull run. While it may not be to the tune of the 6x Nifty saw between 2003 to 2008, even a doubler in next few years may be much more than what many seem to be anticipating at the current juncture.

On the other hand, there is the economy and all the dire calls about how the ballooning of the Federal Balance Sheet means that we don’t have as many bullets as we had earlier. But this has been heard of before. A perma bear in the US projected in 2011 a best case upside of 3.4% for S&P 500 and worst case being negative returns. The reality turned out to be a CAGR of nearly 14%.

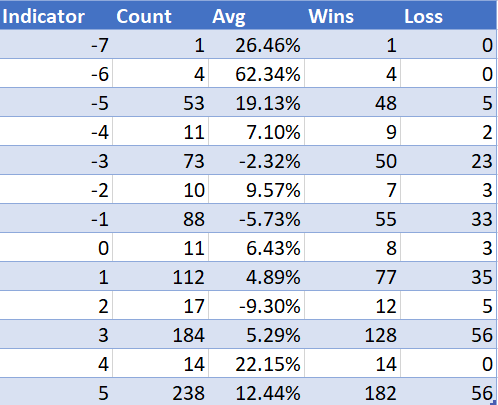

Having said that, even a broken clock can be right twice a day and it’s possible that markets may have found a new peak from where the only path is downwards. To get a better estimate other than valuations, I have been working on what I call “Weight of Evidence” Indicator. Basically it’s a Indicator build using a combo of Trend, Breadth and Sentiment Indicators. The Indicator as of now moves between the range of -7 to +7 and currently stands at 5.

What is interesting is the future returns when the Indicator is at a certain level. We moved to +5 this week. In March of this year, it was -5. The table below outlines the average one year return and the number of times the indicator has reached those levels (Weekly data points, Time frame being 2005 to 2020).

Not surprisingly we can see that when the Indicator is extremely negative (-5 to -7), the future returns are strongly positive. But markets have been there for only 7% of the time. On the other hand, the next best set of returns are when the Indicator is between 4 and 5. Basically while on the negative side, Markets are mean reverting, on the positive side it seems that momentum begets momentum.

Of course, as the data also shows, this indicator has its fair share of failures. When it has reached 5, only 75% of the time has the market been positive at the end of year 1 from that date while 25% of the time it has ended in losses.

One of the things I have learnt in my years in the market is that the upside generally is a surprise even to the most bullish analyst. Buying when blood is on the streets is a great philosophy, but as even Buffett actions recently showcased, it’s not easy to buy especially when the cost of failure can be very high. Buying when the coast is more clear could be a better strategy for those who missed out on the earlier opportunities.

Have a different view with respect to the article. Any frequency based analysis, is highly prone to absence bias. If an event has never been seen, the stats (frequency) records that event as improbable. My understanding is, when the range is -7 to 7, other entries like +8 etc has never been recorded. But that entry of 8 can be the black-swan, one we have never encountered before. Till date, we had never seen a PE >= 30. But current PE is 32! So the frequency distribution curve, would have indicated a blaring sell sign, which it still does, at PE – uncharted waters as colloquially put, but the ship is still steady. Frequency based analysis and conclusions are prone to errors, when the underlying is a factor of rational (or irrational) behavior.

Momentum begetting momentum, is akin to having the moth towards the flame and as is usual, it is not ‘if’ the moth will be singed, but ‘when’. Perhaps, now is the time to exercise caution and leave some profit on the table, as wise investors recommend, and cash out the chips in hand.

What is the conclusion that this article making?