If you were to analyze Mutual Fund assets under management, you shall find it dominated by essentially two styles – the Multicap which now thanks to new rules is changing over to Flexi Cap and Large Cap.

This isn’t much different from what we have seen elsewhere in the word. Large Cap is basically preferred for its lower volatility and ability to be able to absorb a larger pool of capital vs the small and midcap category. The Multicap is where the bet is on the fund manager more than the category.

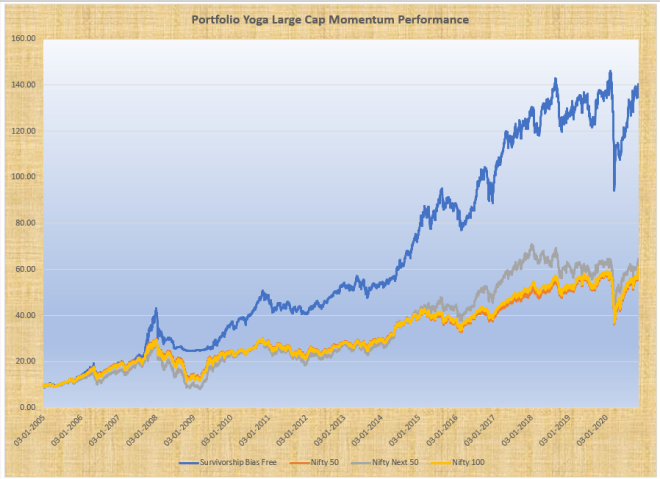

The Portfolio Yoga Large Cap Momentum runs the same algorithm that drives the Portfolio Yoga Multi Cap Portfolio with the only difference being in the Universe of selection. Rather than have the entire market as the Universe as is the case with Multi Cap, with the Large Cap, we restrict ourselves to the 100 largest market capitalization companies.

The NIFTY 100 Index represents about 76.8% of the free float market capitalization of the stocks listed on NSE as on March 29, 2019. Our Portfolio will select stocks from this Universe while applying the same filters and logic as we apply elsewhere.

The Portfolio is a Equal Weight Portfolio of 20 stocks that shall be rebalanced Monthly. We estimate a low churn compared to the Multicap Momentum Portfolio. While one can invest a lower sum that what we recommend, we recommend you invest a minimum of Rs.2 Lakhs in the fund.

Backtest of the Large Cap Portfolio

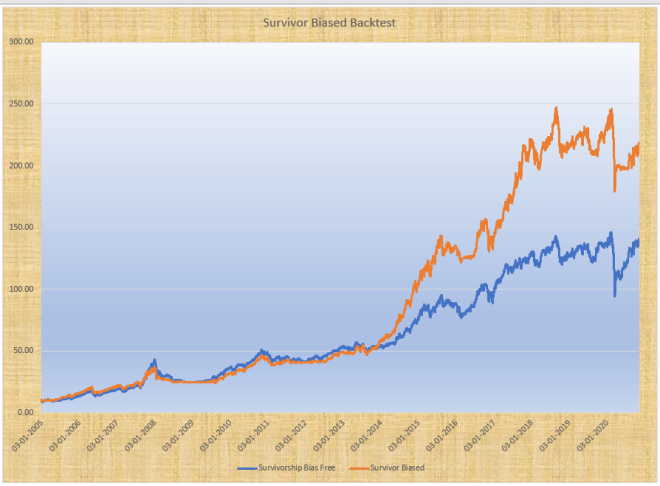

When backtesting a portfolio that takes all stocks as the Universe, the only requirement is to ensure that dead stocks of today are available for selection in the day when selection is made. But when dealing with a subset of the data – an Index for example, not only should the data exist but also one should pick up only stocks that fulfill the criteria as on that day.

Idea for example is today close to a penny stock. But back in its heyday not only was it one of the top 100 stocks but also the top momentum stock. The constituents of most Index go through changes twice a year. Thankfully NSE provides the complete list of stocks that were part of the Index in historical times making it possible to recreate the Index as on those dates.

Creating and backtesting is a painstaking process but one that is absolutely necessary. The difference between testing on the current set of stocks that constitute the Index and the historical can boost up historical returns by a factor of nearly 2 times the return you would generate if you used the correct constituents.

The above chart showcases the equity curve if you used the Current Nifty 100 constituents vs using the Constituents available at the time when rebalancing was carried out. As you can see, Survivor Biased trumps Survivor Free. If only we had an Almanac to the future 🙂

Beating the Index is tough – this applies for Mutual Funds as much as much as Individual Investors if the portfolio sticks 100% to the Index itself. For large parts of the time as is seen currently a few stocks are able to move up the Index higher without the active participation of other stocks.

If beating the markets is tough if not impossible, why should one bother investing in the portfolio would be a question that can crop up in your mind. Why not go with a simple Index Fund where the tax is advantageous and the work much lower.

The answer lies in the fact that while the strategy will always outperform the Index, it has its moments when it does and does in a big way. Of the 189 months for which we have conducted a back-test, the Strategy wins nearly half the months while the other half is won by the Index. But if you look at the complete performance over the entire cycle, you shall see that the Strategy outperformed the Index comprehensively.

Long Term Charts are used everywhere for a reason – they hide the short term glitches that abound. Same is the case with the above chart as well. Rather than just stop with a one chart that contains 15 years of data, let’s break it down to rolling return charts. The back-test data file has the charts and the data backing it up.

Observe closely the 3 year rolling returns. For most part, the Strategy has outperformed all the other available Indices but the difference is not major in recent times.

But if you move to the 5 year rolling returns chart or the 7 or even the 10 year rolling returns chart, the outperformance is pretty evident.

What this means is that while the strategy may not outperform the underlying in the short duration but as you extend the duration, the outperformance starts to showcase itself. While the portfolio can be invested by anyone, I believe that it holds a great value to investors who are new to the concept of Momentum Investing. Investing in well known stocks is mentally easier than investing in stocks that have great momentum but are unknown.

The entire data set is available here {Link}. Do let me know if you have any questions in this regard.

The current open positions of the portfolio is available on the Google Spreadsheet shared with you. The first rebalance will come up at the end of this month.

Finally the BIG Question I think which will crop up in many minds. Should I have both the Portfolios?

My Answer is No.

The underlying strategy being the same, the correlation between the two portfolios will be high. The Large Cap Momentum will have a lower churn compared to the Multi Cap. It from the back-test also has a lower Volatility. Max Draw-down similarly is lower for the Large Cap Portfolio vs the Multi Cap Portfolio. Sector Concentration is lower for most of the time in the Large Cap Portfolio.

All these benefits come with a trade off that the returns will be lower. The backtest CAGR over the 15 years for Multi Cap comes to 24% while its 18% for the Large Cap Portfolio.

The Multicap Universe benefits from its ability to move into the Mid and Small Cap universe and hence take advantage of the Size Factor (which is basically Beta). The downside is that we will have a few bummers on the way that could even make one question the thesis as a whole.

If you are comfortable with allocating money to stocks that are lower down the pecking order in terms of market capitalization and also willing to suffer a higher churn ratio, go for the Multicap Portfolio. On the other hand, if you want to be invested in the best of the Indian Companies and have a lower churn ratio, go for the Large Cap Portfolio.

Either way, we believe that to really showcase the advantages of an approach such as Momentum, you will need to be invested for at least 3 to 5 years. Please mail me if you have any questions with regard to either portfolios.

Is this based on subscription ? How can one replicate it. Is this a fee based service ?

Yes. You can replicate by buying a single lot of all the securities mentioned.

The fee charged is not per Portfolio but all Portfolio’s combined.

Will Asset Allocator tool not used in momentum, as it shows presently to not be much in equity?

Asset Allocation is at the top level. Portfolio is a subset of that.

Can you share the spreadsheet?

Sorry, its part of a paid service.

Is you have smallcase

Not at the moment.

When is the value factor based portfolio coming up?

Hopefully in a month or two. Won’t be a systematic approach though.