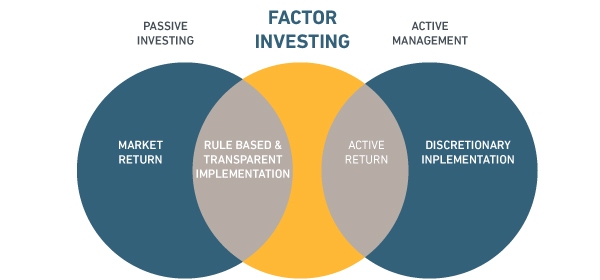

Factor investing hasn’t got of to a start in India even though most people talk about factors. Value based on how you derive it is a factor that could be used as a way to rank stocks and buy the cheapest.

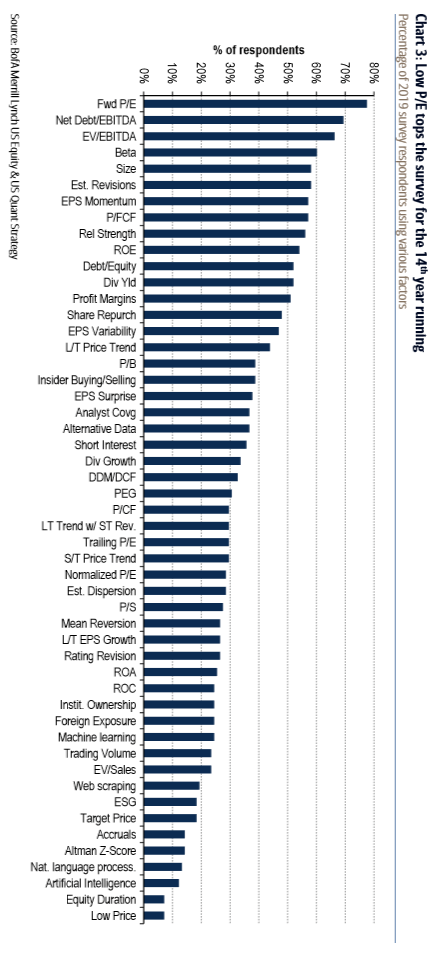

The following chart is from US where the Value factor primarily defined by buying stocks that are cheap as measured by Forward Price by Earnings has been under-performing the market for close a decade now. Yet, its the one that is the most popular. Maybe fund managers are hoping that at some point it shall mean revert and start to be great again.

The fact that interests me most about factor investing in India is the virgin nature of the concept. Most fund managers are happy to chase stories even though reading books on behavioral finance teaches us as to how easy its to get misled through stories weaved by crafty promoters.

Factors on the other hand being totally quantitative, its easier to overcome our challenges for the data stares right back at us. The best book to read on building such quantitative based strategies would be What Works on Wall Street by James O’Shaughnessy

Which of the above factors do you think makes logical sense and which don’t?

Most of the factors used in this approach are derivatives for instance forward PE. The question which I have is price as a forward is forecasting and earnings growth is too then my guess is better than any one else’s or vice versa.

I think a better approach is to narrow down to basics in this approach. Have key PnL, BS, CF items. For instance I would like Operating Revenue, Operating Margin and PAT from the PnL. I would pick a metric of ROIC which though a derivative picks key items from both PnL and BS – Earnings, Expenses, Fixed & Current Assets, Current Liabilities, Cash & equivalents, Tax rate.

For me its been a very simple approach on 3 items from PnL, ROIC, Leverage and most importantly stock price. A company can go into a consideration set because of price momentum and is easily eliminated because of these small factors. There is some discretion but I am not sure whether its good or bad.

Using historical factors which I use along with price is actually momentum investing based on factors. I have not yet made up my mind on chasing low valuations in India as a factor. There is usually a reason why valuations are low for a company. To value chasers it appears that their assessment of value of a company is right and not a collective group of people in the market. The market reflects value via price. Basically being a contrarian is being proven right sometime in the future (maybe not always) but being invested with stocks which are giving portfolio returns with low volatility is what I feel is right or at least comfortable in. There is no need to be married to a stock which happens inherently in value investing. Waiting for a company to fall in valuations (via higher earnings or stock price fall, usually the latter) is timing the market said in a different way.

Anyways what matters is CAGR of portfolio and nothing else 🙂