In my last post titled “Throwing Spaghetti Against The Wall” I showed how after picking up 3 portfolios whose stocks were randomly picked, I could still beat the overall return of the market over a time frame of 10 years.

In continuation of the same, I decided to to a double blind test on picking random portfolios and comparing them to the returns Index gave. I randomly selected 1 date in a year and on that date randomly selected 25 stocks (all done through Excel so as to avoid any bias creeping in).

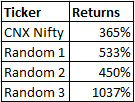

I did it for the years through 2005 to 2010. The results can be downloaded from here (Link). To summarize the same, Random portfolio created beat the Indices in 3 out of the 5 years, in 1 year it under-performed Nifty and Mid-cap while out-performing Small cap Index and in one year has under-performed all other indices.

But if one were to take the final tally, the net results beat the results of all three indices comfortably.

The question that comes thus is, is it a real waste to spend time, energy and money trying to analyze companies? Well, to me, it isn’t so if you believe that you are the 5% of the achievers when the rest of the 95% under-achieve. But if you aren’t sure and your bank balance (from trading / investing and not Salary / other Income) doesn’t seem to show that, its not too late to admit and get back to doing what we do best.

Do note that the only filter I have used was to select stocks that had closed the previous day above 50. It did not matter for me whether they were bullish / bearish based on technical parameters or whether they were fundamentally strong or not based on value analysis. Its pure random selection.

The reason why its tough to believe and even tough to implement this in real life is that we are all suckers for stories. We want a solid reasoning (that resonates with our mind) that comforts us that despite the fact that our investment is deep under water, its not we who are to blame but market forces and the desertion of lady luck.

The whole financial industry is build on this story that you can be better than the markets though not everyone can be above the average (statistically impossible, eh? ), the story has takers (as can be evinced from the number of Mutual funds to PMS to Hedge Funds who offer to take care of your money for a small fee).

In US, it seems for the first time in decades (if not more), people are finally getting out of active strategies and investing into passive ones (ETF’s that provide market returns with minimum fuss and very low charges). Here in India we do lack the spread of ETF’s that are available in US, but I believe that over time, we should see more and more ETF’s hit the market and that would enable investors to invest without having to pay through the nose and yet end up with more or less the same return (or heck even lower).

The reason random portfolio works has nothing to do with selection (after all, we aren’t selecting) but with the concept of compounding. If you were to look at the excel sheet, you shall notice that its not the number of winners that count, but the returns outliers have been able to deliver.

For example, in the portfolio of 2009, the biggest winner was Vakrangee Software. This one stock was able to return the whole capital in affect making the other 24 stocks free.

Warren Buffet has made his money not because he was able to pick all the right stocks, but because some of the stocks he has picked has been multi-baggers to a extent that it wipes off the losses of the few stocks (or should I call business since he having grown so big rarely picks up small stakes and instead wants to get fully into the company) where he called it wrong (and he has several wrong calls).

Markets grow in fits and starts, but in the long term, growth is there for sure (unless you believe that the India story is done with and we shall see a phase such as one seen by Japan). Long term some business will grow at a pace more than others and if we are lucky to have them in our portfolio, our returns should at the very least equate to market returns and at best out-perform the other asset classes easily. And all this without having to burn mid-night oil on what stock to buy, when to buy, when to sell and a thousand other loaded questions.

And before I conclude, do read about how funds rated as Gold can under-perform and many rated neutral / negative outperform (Link). If companies that spent thousands of man hours analyzing in depth funds cannot distinguish the bad apple from the good, what are the chances we can?