We have hundreds if not more number of studies that has shown that over the long term, the best growth is delivered only by equities. While in India, Real Estate has also proven to be a bonafide wealth generator, I strongly believe that growth over the next decade or two will more likely come in Equity with Real Estate more or less providing sub-optimal returns.

So, how does one go about in investing into the markets. For a lay man, there lies there options of investing his savings into the markets

1. Investing via a Mutual Fund

Theoretically speaking, this is the easiest way to gain exposure to the markets. But then again, not all Mutual Funds are the same and hence some amount of research is necessary to ensure that we invest in the funds that have showcased long term growth vs chasing funds that have made a mark in the very near past.

While most mutual funds in United States haven’t been able to beat the benchmark consistently, in India, we have hordes of fund managers who have beaten the benchmark returns year after year. Whether this is due to they being Genuis or whether its because of the fact that the benchmarks are not really that good a criteria to compare against is a story for another time.

But having said that, its a fact that top funds keep changing over time. Prashant Jain is a much acclaimed fund manager, but lets face the facts – his top fund, HDFC Top 200 has generated a CAGR return of 13.36% DSP BlackRock Micro Cap Fund which over the same period has seen a CAGR return of 24.5%.

What I have done above is known as Selection bias. I have selected the DSP fund not by foresight but by using current returns. In 2008 and 2009, the best large cap fund (5 year returns) was Reliance Growth Fund. Over the last 5 years, this fund has provided a CAGR return of 12.8%.

Over a similar period Nifty Total Return Index has shown a CAGR growth of 11.68%. While one can still argue about there being a alpha out there in funds such as HDFC Top 200 and Reliance Growth, we need to also consider the fact that they hold stocks outside of Nifty constituents and in essence, comparing the performance to Nifty is erroneous.

Personally my family is invested into multiple funds across the spectrum and overall, returns have been decent enough. As Warren Buffet once said, diversification is the only free lunch and this applies to Mutual funds as well.

A step above Mutual Funds comes a more personalized investment vehicle.

Portfolio Management Scheme (PMS for short):

Those who follow me on Twitter know that I am a very strong skeptic of PMS as a investment vehicle. My main objection comes from the fact that for most brokerage led PMS, this is not something where the objective is to generate above market returns for the client but is a nice way to churn the portfolio as much as possible in an attempt to garner as much brokerage as can be culled from the account.

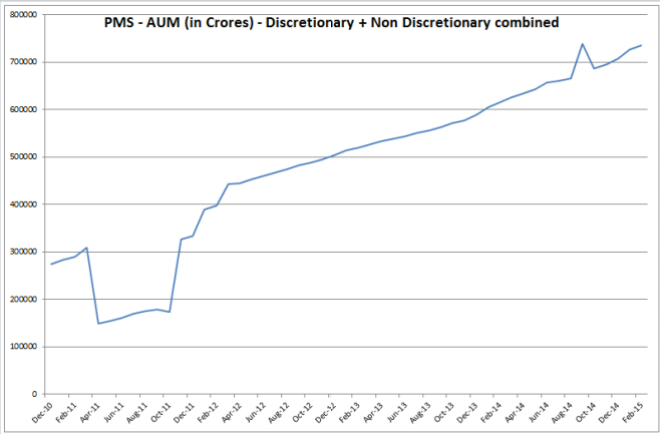

In fact, it is a surprise that Assets under Management of PMS has growth substantially over the years despite most of them not even providing decent returns (let alone market beating) and worse of all, hiding the facts from the potential investors.

I do not have the break-down as which firm manages what amount, but just as a simple exercise, lets review the performances of top names in this business

Coming up first would be Sharekhan (Link)

AUM: Around 32 Crores

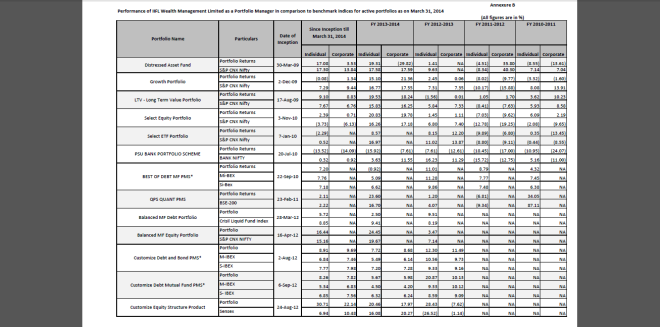

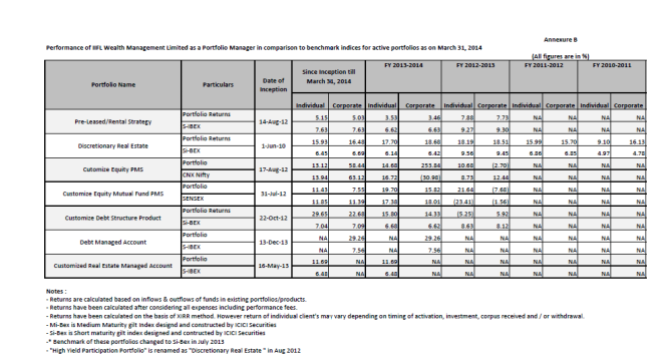

What surprises me is not the under-performance but the fact that NSE Nifty returns are shown as having given different returns when compared with different products.

India Infoline (Link)

AUM: 4600 Crores

India Infoline runs a multitude of funds

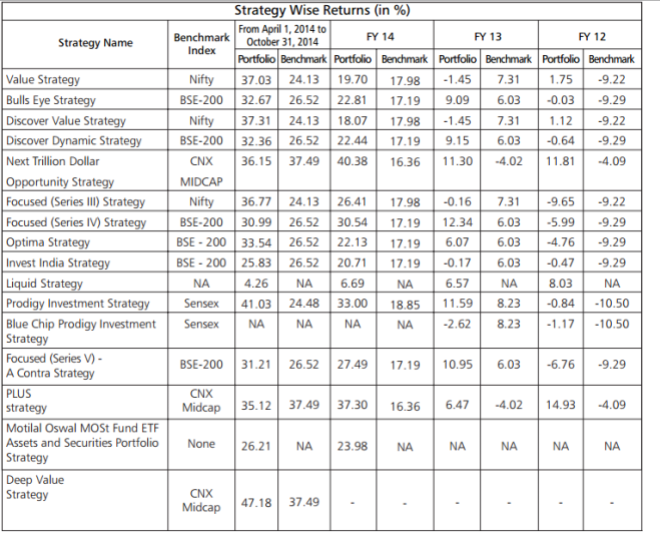

Motilal Oswal (Link)

AUM: 1400 Crores

One of the few which has beaten their benchmarks. But then again, these are 1. Weighted Returns (and not everyone would get the same) and 2. Am not sure if these are after fees or before fees (Fees are substantial in nature, refer to page 14 of the document).

There are at least another 25 – 30 firms offering PMS, but I do hope you get the idea. PMS is not a ideal vehicle to ride the markets. In fact, one PMS firm actually managed to lose money when the markets were going up and lost money when the markets were coming down. The fund manager is now a star investment advisor 🙂

Last but not the least

Direct Investments into Equity:

Directly investing into equities is one of the most risky ways to put savings to work if you are neither willing to work hard nor have a clue about how markets work. Too many folks have burnt their hands in equity investing to swear off anything related to equity (Direct or not). But having said that, the only way to beat the returns generated elsewhere can be found here.

But if you are willing to put in the hours required to learn and understand the various way to analyze the markets, its a effort that can provide for worthwhile returns with total control in your hand.

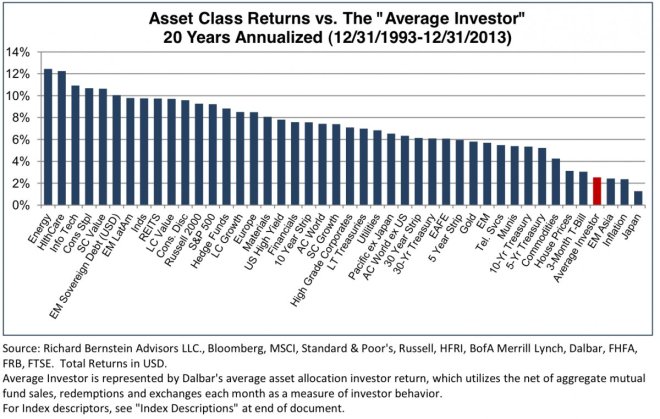

But a caveat first – International evidence has shown that the average equity investor under-performs the markets very badly. In fact, many would have been better off just putting the cash under their pillow than investing into markets

While the above data comes from Mutual Fund investments and redemption by individual investors, with human psyche being the same, direct returns by investors would not be too different.

Investing (no matter how large or small your investments is) is a full time endeavor. Unless you are willing to devote a substantial amount of time, this is definitely not a area to dabble in since not only would the returns be below par, but the time spent could have been better utilized elsewhere.

To fill this gap, we have many a person offering to advise (Newsletter based generally) for a small fee. But with the vast majority of them being pure snake oil sellers, I would generally avoid all such stuff unless they have proof of their pudding (Audited returns of their own funds which in turn should be substantial portion of their net worth)

To conclude, while its true that some funds have shown ability to beat the markets, I recommend novice investors to distribute between a few select funds and a few ETF’s that track the index (Index funds). Invest regularly and you would turn out fine regardless of the gyrations we see in markets.